Divorce Costs Got You Down? Tribal Loans Might Be Your Lifeline

Divorce Costs Got You Down? Tribal Loans Might Be Your Lifeline

Divorce. It’s a word that can send shivers down your spine, conjuring up images of legal battles, emotional turmoil, and, let’s be honest, a hefty price tag. If you’re facing a divorce and feeling overwhelmed by the financial burden, you’re not alone. Many folks find themselves in a tough spot, needing extra cash to cover legal fees, property division costs, and even just everyday expenses. That’s where tribal loans might come into play.

What are Tribal Loans?

Related Articles: Divorce Costs Got You Down? Tribal Loans Might Be Your Lifeline

- Dead Broke? Don’t Let Funeral Costs Bury You: Exploring Tribal Loans

- Cashing In: Navigating The World Of Indian Reservation Loans Online

- Cash-Strapped? The Rise Of Tribal Payday Lenders And What You Need To Know

- Textbook Troubles? Tribal Loans Might Be Your Lifeline (But Read This First!)

- Judgments Don’t Define You: Finding Financial Relief With Tribal Loans

Tribal loans are personal loans offered by lenders affiliated with Native American tribes. These lenders operate on tribal land, which allows them to bypass state usury laws. This means they can often offer higher interest rates than traditional lenders.

Why Are Tribal Loans Gaining Popularity?

The allure of tribal loans lies in their accessibility. They’re often marketed as a quick and easy way to get cash, even if you have less-than-perfect credit. This can be a lifesaver for folks in a bind, especially those facing the financial fallout of a divorce.

Divorce Expenses: A Financial Battlefield

Divorce is expensive, plain and simple. There are court fees, attorney fees, property appraisals, and potential alimony or child support payments. It’s a financial storm that can leave you reeling.

- Legal Fees: Hiring a lawyer is crucial for navigating the legal complexities of divorce. But lawyers don’t come cheap. They can charge hefty hourly rates, and the bill can quickly spiral out of control.

- Property Division: If you’re splitting assets with your soon-to-be ex, you might need cash to buy out their share or cover your own portion of the settlement.

- Living Expenses: Divorce can throw your finances into disarray. You might need to find a new place to live, cover moving costs, and adjust to a new budget.

- Child Support and Alimony: These ongoing payments can significantly impact your finances, especially if you’re the one paying them.

Tribal Loans: A Potential Solution, But Tread Carefully

Tribal loans can be a tempting solution for those facing divorce-related expenses. The fast approval process and easy access to funds can be a welcome relief. But before you jump in, it’s crucial to weigh the pros and cons.

Pros of Tribal Loans:

- Fast Approval: Tribal loan applications are often processed quickly, which can be a huge advantage if you need cash in a hurry.

- Less Stringent Requirements: Tribal lenders often have less strict credit score requirements than traditional lenders, making them an option for those with less-than-perfect credit.

- Flexible Loan Amounts: You can usually borrow a range of amounts, allowing you to tailor the loan to your specific needs.

Cons of Tribal Loans:

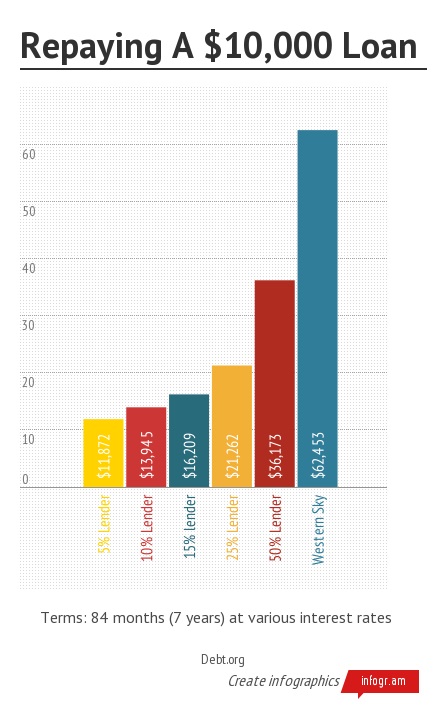

- High Interest Rates: Tribal loans often come with sky-high interest rates, which can quickly add up to a hefty sum in the long run.

- Potential for Debt Traps: If you’re not careful, tribal loans can lead to a cycle of debt. The high interest rates can make it difficult to repay the loan, leading you to take out additional loans to cover the payments, creating a downward spiral.

- Lack of Regulation: Tribal lenders are often less regulated than traditional lenders, meaning there’s less consumer protection in place.

Before You Apply for a Tribal Loan:

- Explore All Other Options: Before you consider a tribal loan, exhaust all other avenues for funding. Can you tap into your savings, borrow from family or friends, or consolidate existing debt?

- Read the Fine Print: Don’t just glance at the loan agreement. Read it carefully, paying attention to the interest rates, fees, and repayment terms.

- Compare Rates and Terms: Don’t just settle for the first tribal loan you find. Shop around and compare rates and terms from different lenders.

- Consider the Long-Term Impact: Think about how the loan will affect your overall financial picture. Can you afford the monthly payments? Will it create a burden on your budget?

Alternatives to Tribal Loans:

- Personal Loans from Banks and Credit Unions: While these loans may have stricter credit score requirements, they often come with lower interest rates than tribal loans.

- Credit Cards: If you have good credit, you might be able to use a credit card to cover divorce expenses. Just be sure to pay off the balance as quickly as possible to avoid high interest charges.

- Government Assistance Programs: Depending on your situation, you might be eligible for government assistance programs that can help you pay for divorce-related expenses.

- Family and Friends: Don’t hesitate to ask for help from your loved ones. They might be willing to lend you some money to get you through this tough time.

Divorce: A New Chapter, A Fresh Start

Divorce can be a tumultuous period, but it also represents an opportunity for a new beginning. While the financial burden can be daunting, it’s crucial to remember that you’re not alone. Seek advice from financial professionals, explore all your options, and prioritize your financial well-being as you navigate this new chapter.

FAQ about Tribal Loans for Divorce Expenses:

Q: Are tribal loans legal?

A: Yes, tribal loans are legal. They are offered by lenders operating on tribal land, which allows them to bypass state usury laws.

Q: Are tribal loans safe?

A: The safety of tribal loans is a matter of debate. While they are legal, they often come with high interest rates and lack of regulation, which can pose risks for borrowers.

Q: What are the risks of taking out a tribal loan?

A: The main risks of tribal loans include high interest rates, potential for debt traps, and lack of consumer protection.

Q: What should I do if I’m struggling to repay a tribal loan?

A: If you’re struggling to repay a tribal loan, contact the lender immediately. They may be willing to work with you on a repayment plan. You can also seek help from a credit counseling agency.

Q: Can I get a tribal loan even if I have bad credit?

A: Tribal lenders often have less strict credit score requirements than traditional lenders. However, this doesn’t mean you’re guaranteed approval. The lender will still review your application and consider your financial history.

Q: What are the best ways to avoid tribal loans?

A: The best way to avoid tribal loans is to explore all other options for funding, such as personal loans from banks or credit unions, credit cards, government assistance programs, or family and friends.

Remember, divorce is a challenging process, but with careful planning and responsible financial decisions, you can navigate the financial hurdles and emerge stronger on the other side.

Closure

Thus, we hope this article has provided valuable insights into Divorce Costs Got You Down? Tribal Loans Might Be Your Lifeline. We thank you for taking the time to read this article. See you in our next article!

")