Ditch the Debt Trap: Smart Alternatives to Tribal Payday Loans

Ditch the Debt Trap: Smart Alternatives to Tribal Payday Loans

Feeling the pinch? Short on cash and need a quick loan? It’s a common situation, but before you jump into a tribal payday loan, hold on! Those tempting offers can quickly turn into a debt nightmare.

Let’s face it, payday loans, especially tribal ones, are notorious for sky-high interest rates and predatory practices. They might seem like a quick fix, but they can leave you stuck in a cycle of debt that’s hard to break. But don’t worry, you’re not alone. There are plenty of safer, more affordable alternatives out there.

Related Articles: Ditch the Debt Trap: Smart Alternatives to Tribal Payday Loans

- Stuck In A Financial Rut? Tribal Loans Might Be Your Lifeline (But Read This First!)

- Stuck With A Prepaid Card? Tribal Loans Might Be Your Lifeline

- Tribal Installment Loans Vs Payday LoansTitle

- Easiest Tribal Loans To GetTitle

- Cash-Strapped? Tribal Loans Might Be Your Lifeline

This article is your guide to understanding why tribal payday loans are risky business and to exploring the best alternatives that can help you get back on your feet financially.

What are Tribal Payday Loans?

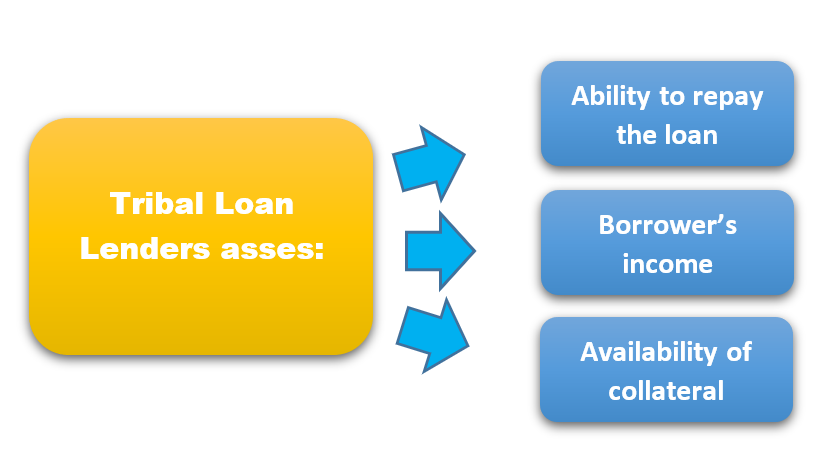

Tribal payday loans are offered by lenders who are affiliated with Native American tribes. These lenders often operate on tribal land, claiming sovereign immunity to avoid state regulations that govern traditional payday loans.

Here’s the catch: While they may seem like a loophole, tribal payday loans often come with the same high interest rates and hidden fees as their non-tribal counterparts. They can also be difficult to navigate, leaving borrowers with limited recourse if something goes wrong.

Why are Tribal Payday Loans So Risky?

- Sky-high Interest Rates: Tribal payday loans typically charge interest rates of 400% or more, which can quickly spiral out of control.

- Hidden Fees: These loans often come with a variety of fees, such as origination fees, late fees, and rollover fees, that can add up quickly.

- Predatory Practices: Some tribal payday lenders use aggressive tactics to collect on their loans, including harassing borrowers and reporting them to credit bureaus.

- Lack of Regulation: Because tribal lenders operate on sovereign land, they often avoid state regulations, making it harder for borrowers to seek protection.

- Debt Traps: The high interest rates and fees can make it difficult for borrowers to repay their loans, leading to a cycle of debt.

Alternatives to Tribal Payday Loans: A Breath of Fresh Air

1. Credit Unions: A credit union is a member-owned financial institution that often offers lower interest rates and more flexible repayment terms than traditional banks. They also tend to be more understanding of borrowers’ financial situations.

2. Community-Based Organizations: Many non-profit organizations offer financial assistance programs, such as emergency loans, budgeting counseling, and debt management services.

3. Payday Alternative Loans (PALS): These are short-term loans offered by some credit unions with lower interest rates and longer repayment terms than traditional payday loans.

4. Personal Loans: Personal loans can be a good option for larger expenses, such as medical bills or home repairs. They typically have lower interest rates than payday loans and can be repaid over a longer period.

5. Family and Friends: If you’re in a pinch, consider reaching out to family or friends for a loan. This can be a good option if you’re comfortable with the terms and can repay the loan promptly.

6. Online Lending Platforms: Online lending platforms can be a good option for borrowers with good credit. They often offer lower interest rates than traditional payday lenders and can be a convenient way to access funds.

7. Cash Advance Apps: Cash advance apps allow you to borrow small amounts of money against your next paycheck. These apps are typically free to use, but they may charge fees for early access to your funds.

8. Sell Unwanted Items: Selling unwanted items online or at a consignment shop can be a quick way to raise cash. You can even consider selling items you don’t need anymore, like old electronics or clothing.

9. Negotiate with Creditors: If you’re struggling to make payments on your existing debts, reach out to your creditors and see if they’re willing to work with you. You may be able to negotiate a lower interest rate or a payment plan.

10. Consider a Side Hustle: If you need extra cash, consider taking on a side hustle, like driving for a ride-sharing service, delivering food, or freelance writing. This can be a good way to earn extra income while you’re getting back on your feet.

Beyond the Alternatives: Building a Solid Financial Foundation

1. Budgeting: Creating a budget is the first step to managing your finances. Track your income and expenses, identify areas where you can cut back, and create a plan for saving and paying down debt.

2. Emergency Fund: Having an emergency fund can help you avoid taking out high-interest loans when unexpected expenses arise. Aim to save at least three to six months’ worth of living expenses.

3. Credit Score: Your credit score is a key factor in determining your interest rates on loans. Work on improving your credit score by paying your bills on time, keeping your credit utilization low, and avoiding late payments.

4. Financial Education: Take advantage of free resources available online and at your local library to learn more about personal finance. Understanding your finances will help you make informed decisions and avoid costly mistakes.

5. Seek Professional Help: If you’re struggling with debt or have difficulty managing your finances, don’t hesitate to seek professional help. A credit counselor or financial advisor can provide guidance and support.

Don’t Let Debt Trap You: Choose a Better Path

Choosing a tribal payday loan might seem like the easiest option when you’re in a tight spot. But remember, it’s a quick fix that can lead to a long-term financial burden. Instead, explore the alternatives, build a solid financial foundation, and take control of your finances. You’ll be glad you did!

FAQ About Tribal Payday Loan Alternatives

Q: What if I have bad credit?

A: Don’t despair! Even with bad credit, you have options. Credit unions and community-based organizations often offer loans to borrowers with less-than-perfect credit. You can also try online lending platforms that specialize in loans for borrowers with bad credit.

Q: How do I choose the best alternative for me?

A: Consider your financial situation, the amount you need, and the repayment terms offered by each lender. Compare interest rates, fees, and repayment periods to find the best option for your needs.

Q: What if I’m already in debt from a tribal payday loan?

A: Don’t panic! There are steps you can take to get out of debt. Reach out to a credit counselor or debt management agency for help. They can negotiate with your creditors and help you create a plan to repay your debts.

Q: Is it legal to take out a tribal payday loan?

A: While tribal payday loans are legal, they are often controversial due to their high interest rates and predatory practices. It’s essential to understand the risks involved before taking out a tribal payday loan.

Remember, you’re not alone. There are resources available to help you navigate your financial challenges and find a path to financial stability. Take control of your finances, explore your options, and choose a path that leads you toward a brighter financial future.

Closure

Thus, we hope this article has provided valuable insights into Ditch the Debt Trap: Smart Alternatives to Tribal Payday Loans. We appreciate your attention to our article. See you in our next article!

")